Being investigated by the Department of Labor (DOL) can be a nerve-wracking and time-consuming experience for any benefit plan provider. However, being familiar with the DOL’s investigation flow and preparing properly can make the process more efficient and less painful.

The Investigation Process

Initiation Letter and Res ponse

ponse

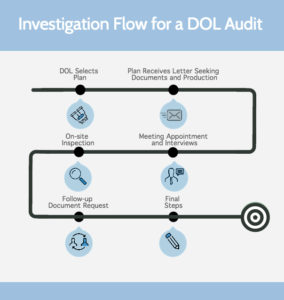

After the DOL has selected a benefit plan for an investigation, they send out an initiation letter. This letter contains a request for specific items and documents that they need to conduct the audit. It is common for the list of requested items to be several pages in length.

Common items that are requested include:

- Plan and trust documents

- Plan policies/procedures

- Summary Plan Description (SPD)

- Meeting minutes

- Form 5500 annual reports and associated documents

The letter also includes the timing of the investigation and the period of time covered. It is possible to be given a shorter time frame, typically ten business days, to produce the requested documents. It is also possible that the request covers the previous three years or more.

It is important to not view a gap in time after you produce the documents as a “clean bill of health” from the DOL. It is entirely possible for several months to elapse between audit stages.

Practice Pointers

- If the letter requests that an auditor inspect the documents on-site, ask if you can send the documents to the investigator directly. This is often more efficient, less disruptive and makes it easier to keep an accurate record of the information you have provided.

- If the timeframe they give you is too short for you to make it work, contact the DOL agent and request an extension of time.

- Consider offering to produce some of the documents in advance of the initial deadline as a good faith gesture.

- Appoint an internal “point person” who is responsible for gathering all of the documents and information.

- Only produce what the DOL requests and be prepared for follow-up requests.

- Coordinate with the DOL investigator regarding the production format. They may require or prefer electronic submission as opposed to paper.

- Ensure that you get some type of delivery confirmation or return receipt.

- Request the return of all materials after the investigation is closed. The DOL can refuse to return copies, but they are required to return originals.

Meeting Appointment & Interview

The next step in the investigation flow is the meeting appointment and interview stage. The DOL will most likely request to interview one or two trustees. They may require depositions but typically they are voluntary interviews. Legal counsel may be present during the interview, but their role will be limited.

Interviewees can expect a review of personal background information before the more specific questions start. These questions could relate to the documents that were previously provided.

Practice Pointers

- Review the DOL’s enforcement manual prior to the interview. This manual serves as a roadmap for DOL investigations including the interview process.

- Prepare for the interview by reviewing plan operations and basic procedures.

- Review your plan’s policies.

- Know your plan’s history and any significant events.

- Be careful to only respond to questions that are asked. Don’t volunteer any additional information.

- It is acceptable to answer with “I don’t know” or “I don’t recall” if it is an accurate response.

- Treat the interview like a deposition and act accordingly.

On-Site Inspection

The next phase is the on-site inspection. The DOL will identify the date on which the inspection will take place.

Practice Pointers

- Stick to the scheduled date(s) and avoid rescheduling.

- Make it a priority for the entire office to be clean and presentable.

- Set aside a designated room for the investigator. In the room, ensure that the records are organized and that the investigator is comfortable.

- Do not allow the investigator to roam freely around the office.

- Limit the investigator’s interaction to just the designated point person. Do not allow impromptu interview sessions with other staff members.

- If the agent requests additional documents, pursue delivery at a future date so you can allow your legal counsel to review.

- If you do provide additional documents during the inspections, make copies and keep a record of what you provided.

DOL Response and Communication on Progress of Audit

Once the investigation has been completed the investigator will compile their findings into a final letter. The timing on this can range from a few weeks to years from the first date of contact.

There are three general types of letters that can be received:

- No Violations Letter

- 10-day Voluntary Compliance Letter

- Referral Letter

No Violation Letter

If you receive this letter it means that the case is closed and no violations were found.

10-day Voluntary Compliance Letter

If the DOL identified any issues during their investigation the letter will detail the alleged problem(s) and identify the proposed correction(s). The letter may also identify possible penalties. The Employee Retirement Income Security Act of 1974 (ERISA) dictates that a 20% penalty be imposed for certain damages.

A written response is normally required within 10 days, but you may receive an extension if necessary. The DOL may also refer you to the IRS if excise tax is due.

Referral Letter

This letter can be a referral to a solicitor, the IRS or the DOJ. These letters are generally only received for specific matters, such as:

- If the proposed correction will take a long time

- If there are possible fraud or criminal charges

- If a fiduciary needs to be removed

- If there is a unique or complex ERISA violation

- If there is a violation of other laws

Practice Pointers

- Coordinate with your fiduciary liability insurance carrier

a. They may prefer to pay to remedy the issues rather than paying the legal fees to dispute them.

b. Keep in constant communication with them. Do not agree to a monetary settlement without their approval. - Consider seeking an extension if the correction is time consuming or if the plan might challenge all or some of the DOL’s conclusions.

- Consider a tolling agreement (if not already implemented) to eliminate the sense of urgency. The DOL may try to raise statute of limitations issues.

- Seek a resolution that avoids admitting fault and avoids penalties under ERISA section 502(I).

- Seek to resolve without a settlement agreement since ERISA section 502(I) penalties apply to settlement agreements.

- If negotiations with the investigator are deadlocked, seek to discuss with the regional office director or the national office.

- If the plan corrects a prohibited transaction, excise taxes may be owed to the IRS.

a. The fiduciary insurance may need to pay the excise tax. You cannot use plan assets to pay this.

While being investigated by the DOL is never a pleasant experience, being prepared can make a huge difference from the very start. Knowing what to expect can help minimize confusion and help the entire process move along more smoothly. If you have any questions or concerns, please contact one of our employee benefit plan specialists.

Written By: Glenn M. Eyrich, CPA | Partner and John E. Mossberg, Shareholder | Reinhart Boerner Van Deuren S.C.